Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.

Summer showers and shipping setbacks: a perfect storm for UK retailers?

We're known for complaining about the weather in Britain, but retailers in particular have good reason to. And their complaints don’t stop there…

We have passed the longest day of the year and the evenings are progressively drawing in. But what happened to summer? The confluence of sporting events may have distracted us, but the reality is that rain and overcast skies characterised our June and early July.

As irritating as this was for us all, the effect it had on consumer behaviour is even more frustrating for companies trying to convince us to part with our cash. Unseasonal weather not only impacts traditional clothing and footwear purchasing patterns, but also appetite for leisure spending.

On-the-ground feedback

Sometimes the small-cap equity arena can be the best place to hear early indications of what businesses are experiencing. From monitoring this space, we have noticed a recent uptick in companies flagging the cold and wet weather as a contributing factor to disappointing retail sales.

As an example, UK budget footwear retailer ShoeZone* referenced weaker-than-expected spring/summer sales from April to June due to unseasonal weather.

From footwear to footfall, we’ve also seen evidence of the bad weather impacting foodservice outlets via UK wholesale retailer Kitwave*. Along with other operations, this company supplies food and beverages to independent hospitality customers such as cafés, small restaurants and pubs. In its latest update, Kitwave cited lower-than-expected demand in the foodservice hospitality customer base in H1. Many of these outlets are in parks, zoos or other leisure locations, which are apparently experiencing lower visitation because of on/off rain this summer.

This is early-stage feedback; more clarity should be gained over the next two months as we observe late-summer weather and consumer discretionary companies report. In the meantime, we turn our attention to other factors that could spoil the next retailer reporting round.

Shipping adds to woes

As well as dampened demand, the latest company comments on input cost inflation are also cause for concern. Not only are labour-heavy retailers dealing with another round of national minimum wage increases, but the ongoing Red Sea disruption is increasingly affecting their logistics. Because of the attacks by Houthi rebels, cargo ships are having to undertake detours to avoid the pivotal Suez Canal trade route between Europe and Asia. This adds weeks to transport time as well as increasing fuel costs.

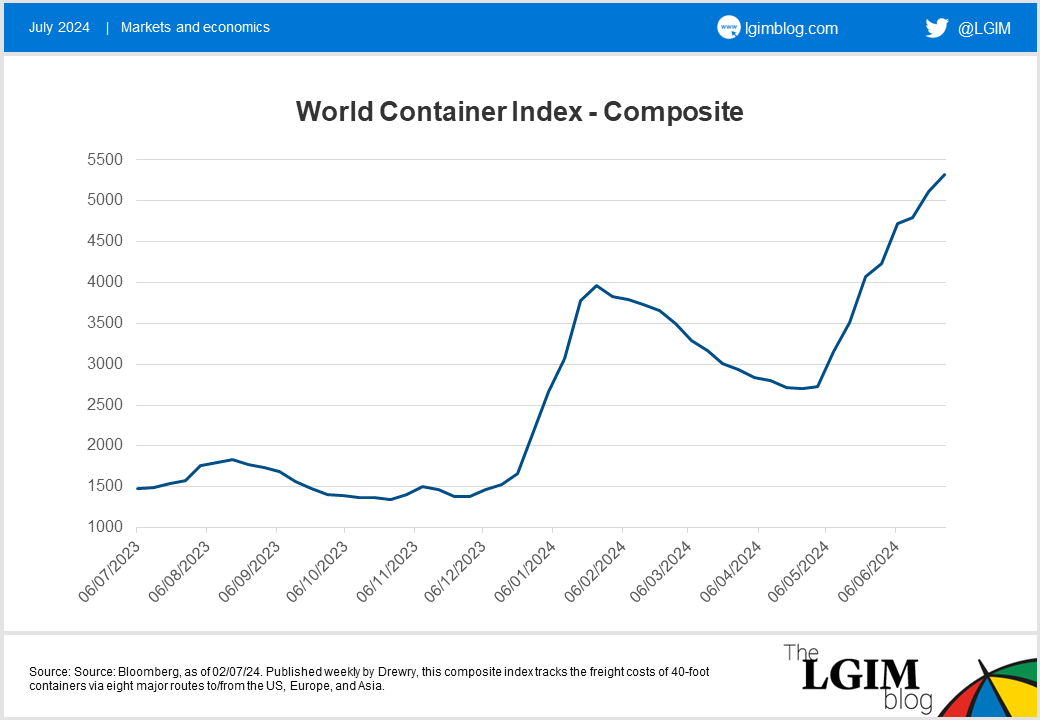

Turning again to our ‘canary in the coalmine’ – small caps – a good example of these delays are recent comments from UK furniture retailer DFS* and UK motoring and cycling retailer Halfords*. This summer DFS issued a profit warning when it confirmed that £12-14m of customer orders have been delayed by the disruption. Also, both DFS and Halfords commented on very significant increases in sea freight rates. This can be seen in the graph below, which charts Drewry’s World Container Index – a widely used benchmark for container freight rates.

The graph shows that the freight benchmark rate has increased by 256% when compared with the same week last year. This is a substantial spike to levels not forecast by companies at the beginning of the year. Hence we are now seeing early communications by companies needing to make adjustments to profit guidance to factor in elevated costs. This conversation is only likely to get noisier into the next reporting round.

There are several reasons behind the spike in global shipping rates. Vessel diversions have led to port congestion as well as fleet capacity constraints. Not only is there a shortage of ships, but there is also a shortage of empty containers. Added to that, underlying market demand has remained strong. Consequently, customers are booking peak-season cargoes sooner than they normally would.

An active and selective approach

Given these demand-side and supply-chain headwinds facing consumer discretionary stocks, we believe an active approach to investing can be crucial to identifying which companies will be most impacted and which have the potential to weather this perfect storm.

For example, two aspects we consider when conducting stock selection are scale and price-point. Companies which are larger buyers can negotiate more favourable shipping rates. Those which have a higher-priced product offering can embed (or pass on) some of the additional costs to consumers. Conversely, smaller size players can be squeezed more easily, and those with value product propositions have less flexibility in their pricing.

*For illustrative purposes only. Reference to this and any other security is on a historical basis and does not mean that the security is currently held or will be held within an LGIM portfolio. Such references do not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

Legal & General Investment Management is one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.