Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.

Cashless in Calcutta

The consensus remains bullish on India even after, or perhaps because of, recent currency reforms. We beg to differ. While Modi’s reform efforts have been impressive, only rivalled by Mexico following the global financial crisis, India still faces significant cyclical headwinds.

Although they may well be beneficial over the medium term, India's currency reforms could be more painful in the short term than markets expect. According to the RBI, out of $220bn in bank notes declared null and void only $15bn had been replaced as of November 21. In a cash-based economy this could have a severe impact on economic activity. Also, given logistical bottlenecks (printing presses), we expect the impact to last well into 2017.

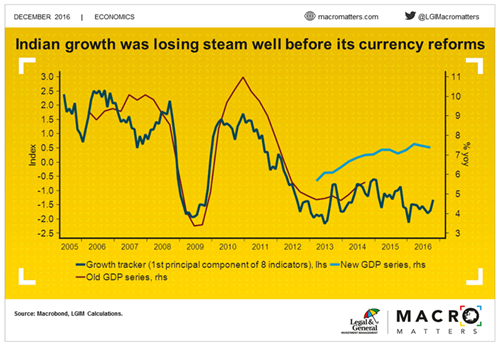

Even before the currency reforms, we believe that India’s economy was doing much worse than official GDP numbers suggest. Industrial production, non-oil imports, and corporate sales were all contracting. This is hard to reconcile with official reported growth rates of 7.5% and we believe that growth is closer to 5.5%. Our growth tracker, based on eight variables, also suggests that the economy was losing steam well before the currency reforms.

The outlook remains challenging. Banks are saddled with high NPLs, which are reducing the impact of lower interest rates, while fiscal policy may end up even tighter than budgeted given a shortfall in privatisation receipts. In addition, the monsoon turned out to be normal, dampening earlier hopes of buoyant agricultural growth. And a large chunk of retroactive civil service pay rises has already been paid, without much impact on activity. Finally, most agree that private investment is in the doldrums, boding ill for the medium-term growth outlook.

Recommended content for you

Learn more about our business

Legal & General Investment Management is one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.