Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.

Wave erosion: lockdown risk could wear down investor sentiment

Until recently, improvements in the treatment of COVID-19, increases in ICU capacity, and a decoupling between death and infection rates – compared with the initial stages of the pandemic – provided us with confidence that severe future lockdowns were unlikely.

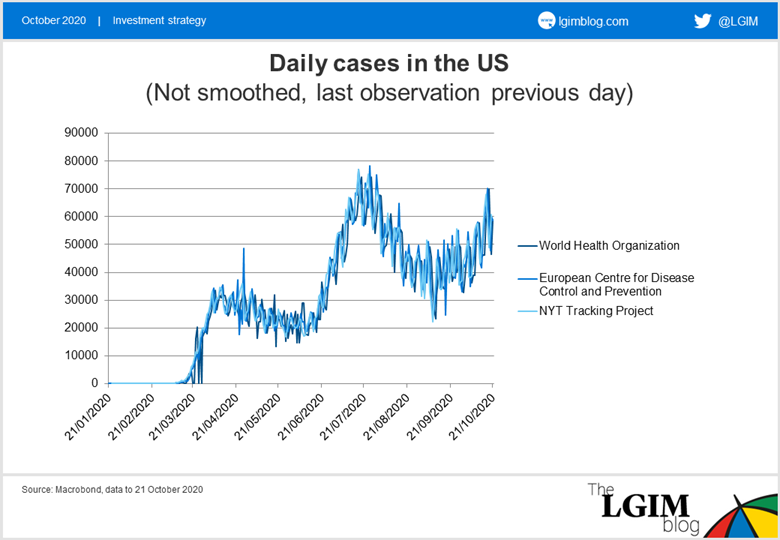

However, we have now become more concerned about the possibility of a second widespread shutdown in the western world. The past week has brought confirmation of stricter restrictions in parts of the UK, Ireland, Belgium, and France to name just a few places. The case load is increasing in the US as well; although the country did not reopen schools to the same extent as in Europe, we believe there will be increased pressure for lockdowns there too.

Conscious of the economic costs of such measures, policymakers have been torn between trying to control COVID-19 and trying to mitigate the economic damage. These are interlinked, of course: tolerating the spread of the virus is more likely to depress than revive economic activity. There are no easy answers.

In our own research, we are looking at the role of schools in spreading the virus, the impact of colder temperatures (which mean, as a minimum, more activity indoors), and the degree of restrictions required to contain the increasing pressure COVID-19 could place on hospital ICUs. The one area of comfort is that the experience of the southern hemisphere suggests the existing measures will likely make this an exceptionally mild flu season. However, the scientists continue to recommend early action to contain the spread and no politician wants to risk pictures of patients on trolleys in hospital corridors if current trends were to persist.

Stay alert

Yet this lockdown risk is underestimated in consensus opinion at the moment, in our view. Investor surveys show that people are preoccupied with the US election and the associated matter of Congress agreeing a fiscal deal; the virus plays second or even third fiddle at the moment.

This seems too complacent to us. We now know the magnitude of the economic hit from lockdowns – even smaller-scale restrictions can devastate sectors like hospitality – and it is far from certain that they will be accompanied by the level of policy support that steadied financial markets in March.

We are therefore becoming slightly more cautious on market risk. We have kept our equity weight unchanged but we are putting in place some protection like hedging the South Korean won.

However, for the medium term we remain inclined to “buy the dip” in equities in anticipation of an early-cycle economy and our conviction around the availability of a vaccine in 2021.

Recommended content for you

Learn more about our business

Legal & General Investment Management is one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.