Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.

Are equities too expensive?

After eight bull market years and with strong macro data all round, recession and bear market memories must surely be fading. Still, signs of exuberance or great bullishness are difficult to find; at most there is cautious optimism. Why? One of the most common push-backs against an equity bull case is that equities are too expensive. I can see where this concern comes from, but believe it’s something to push back against. Here are my top 10 points on equity valuations.

After eight bull market years and with strong macro data all round, recession and bear market memories must surely be fading. Still, signs of exuberance or great bullishness are difficult to find; at most there is cautious optimism. Why? One of the most common push-backs against an equity bull case is that equities are too expensive. I can see where this concern comes from, but believe it’s something to push back against. Here are my top 10 points on equity valuations.

1) Equities valuations are above average in the majority of regions measured on the majority of multiples, but not by much. Across seven multiples and six regions the average valuation is at the 64th percentile of its historic range.

2) Not all equity markets are equally expensive. US equities rightly get the most attention, as they are the biggest market and it’s difficult to imagine US equities correcting in isolation. The average US multiple is at the 87th percentile of its historic range. But the US is an outlier in terms of valuations.

3) While the US Shiller PE has only been higher 4% of the time, the Japanese forward PE has only been lower 12% of the time.

4) Even though the extreme valuation of the Shiller PE worries us, we need to beware of cherry picking! With countless valuation multiples across lots of countries and regions there will always be some that make equities look expensive and others that make them look cheap. We need to look at a range of valuation indicators.

5) We believe that valuations are useless as timing tools. There has been close to zero correlation between PEs and one-year returns. You have been able to buy the S&P on 8.8x earnings and lose 18% of you money over next year and buy it on 29x and earn a 22% return.

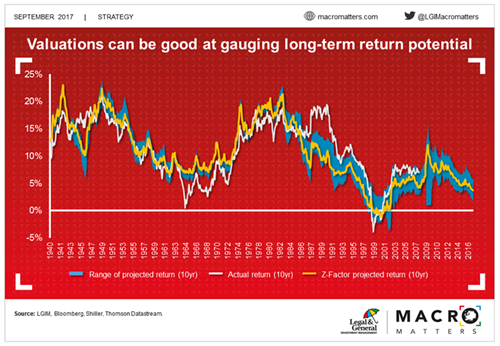

6) We believe, however, that valuations can be a great guide to long-term return potential. They tend to mean revert over longer time horizons, leaving investors’ return potential decided by the dividend yield and earnings growth.

7) Far above average US valuations suggest US equities will deliver below historical average return potential in the future. Our Z-Factor US valuation composite is consistent with 3.7% total returns per annum over the next decade. This is low, but so are bond yields.

8) Equity valuations still look relatively attractive relative to other asset classes in our view. This relative advantage can play out in two main ways. 1) Equities are insulated from rising bond yields, or 2) equities can re-rate if bond yields stay ‘lower for longer’.

9) Bull markets don’t die of overvaluation. Bear markets have started on PEs as low of 8x and as high as 28x…and many levels in between.

10) Higher valuations make for a more painful bear market. Bear market draw downs have been greater when the bull market ended on high valuations

So, equities are no longer cheap, but neither are valuations so extreme that they give a tactical sell signal. High valuations can reduce the long-term expected return of equities and can amplify the draw-down in a bear market. But in our view, they do not provide any insight into the timing of the next bear market.

Recommended content for you

Learn more about our business

Legal & General Investment Management is one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.